Live LTM¶

This notebook creates a model by using only the Python interface, with no file backing.

[1]:

import os

import numpy as np

from pyltmapi import LtmSession, LtmPlot

import logging

logging.basicConfig(level=logging.INFO)

from pathlib import Path

ltm_core_path = os.environ.get("LTM_CORE_PATH", str(Path("~").expanduser().joinpath("ltm/release/bin/")))

license_file = os.environ.get("LTM_CORE_LICENSE_FILE", str(Path("~").expanduser().joinpath("ltm/ltm-license.dat")))

[2]:

from IPython.display import HTML, display, display_markdown

ltmapi_version = LtmSession.version()

display(f"pyltm version {ltmapi_version}")

'pyltm version PyLTM version: 0.25.2'

[3]:

def usercallback(program_info: dict, userdata: any):

print(userdata)

print(program_info)

return True

def generate_plots(ltm):

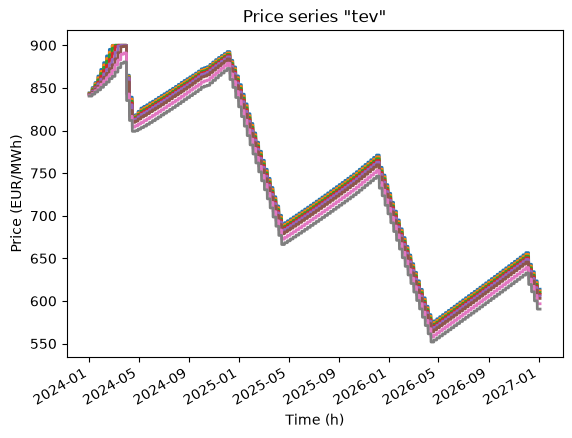

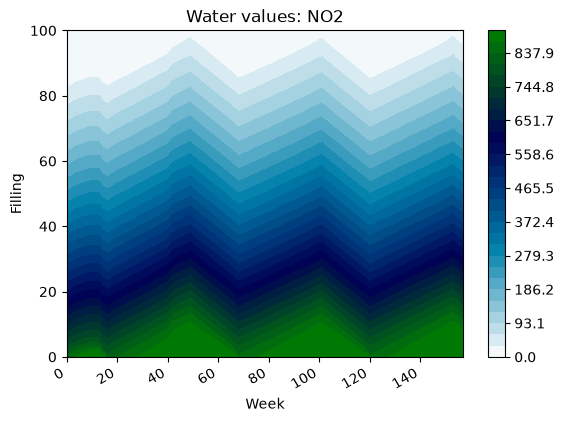

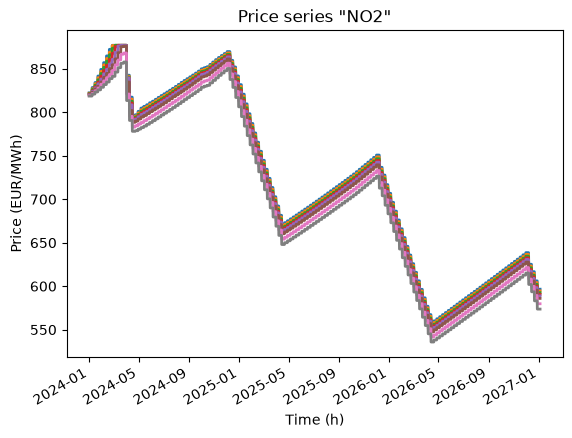

# Water values and price series

for area in ltm.model.areas():

print(area)

if area.have_water_value_results():

# Water values

LtmPlot.make_water_value_plot(area.water_value_results(), area.name)

# Market results

LtmPlot.make_market_results_plot(area.market_result_price(), area.name)

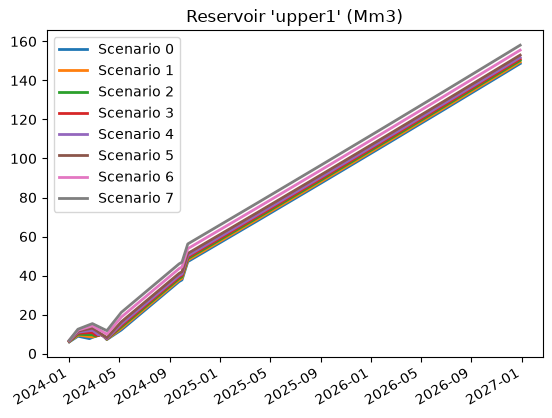

# Detailed hydro results from

for area in ltm.model.areas():

print(area)

# area reservoirs

rsvs = area.reservoirs()

for rsv in rsvs:

LtmPlot.make_generic_plot(rsv.reservoir(), f"Reservoir '{rsv.name}'")

for rsv in rsvs:

LtmPlot.make_generic_plot(rsv.discharge(), f"Discharge '{rsv.name}'")

LtmPlot.make_generic_plot(rsv.inflow(), f"Inflow '{rsv.name}'")

LtmPlot.make_generic_plot(rsv.production(), f"Production '{rsv.name}'")

LtmPlot.make_generic_plot(rsv.bypass(), f"Bypass '{rsv.name}'")

LtmPlot.make_generic_plot(rsv.spill(), f"Spill '{rsv.name}'")

[4]:

from datetime import datetime, timedelta

from pyltm import Txy

[5]:

from pyltm import Area

def add_area(session, name):

area = Area()

area.name = name

return session.model.add(area)

[6]:

from pyltm import DCLine, util

def add_dclines(session, name):

dcline = DCLine()

dc = session.model.add(dcline)

dcline.name = name

dcline.forward_capacity = util.make_constant_txy(200)

dcline.backward_capacity = util.make_constant_txy(200)

dcline.loss_percentage = 2.0

dcline.forward_cost = 5

dcline.backward_cost = 5

return dc

[7]:

from pyltm import Load, Txy

from pyltm import util

def add_load(session, name, capacity: Txy = Txy()):

load = Load()

if len(capacity.timestamps) == 0:

load.capacity = util.make_txy(

[

("2024-W01", [20]),

("2024-W05", [25]),

("2024-W10", [30]),

("2024-W15", [20]),

]

)

else:

load.capacity = capacity

load.name = name

return session.model.add(load)

[8]:

from pyltm import Inflow

def add_default_inflow_series(session):

small = session.model.add(Inflow())

small.name = "small"

small.series = util.make_constant_txy(0.001)

constant = session.model.add(Inflow())

constant.name = "constant"

constant.series = util.make_constant_txy(1.0)

[9]:

from pyltm import Reservoir, Plant, Xy

def create_simple_topology(session):

upper1: Reservoir = Reservoir()

upper1.name = "upper1"

upper1.degree_of_regulation = 3

upper1.regulated_inflow = util.make_txy(

[

("1900-01-01T00:00:00Z", [1.0]),

]

)

upper1.average_regulated_inflow = 10

upper1.max_discharge = 50

upper1.reference_curve = util.make_txylin(

[

("W15", [50]),

("W20", [350]),

("W40", [450]),

]

)

upper1.initial_volume = 5

upper1.tailrace_elevation = 150.0

upper1.gross_head = 800.0

upper1.volume_curve = util.make_volume_curve(

[

(1100, 0),

(1130, 500),

]

)

session.model.add(upper1)

lower1 = Reservoir()

lower1.name = "lower1"

lower1.degree_of_regulation = 0.5

lower1.regulated_inflow_name = "constant"

lower1.max_discharge = 200

lower1.reference_curve = util.make_txylin(

[

("W01", [1500]),

]

)

lower1.initial_volume = 0

session.model.add(lower1)

plant1 = Plant()

plant1.name = "plant1"

plant1.average_energy_equivalent = 1.6

plant1.discharge_energy_equivalent = util.make_txy([("W01", [1.6])])

plant1.pq_curves = util.make_pq_curve(

[

(

"W01",

[

(0, 0),

(50, 200),

],

)

]

)

plant1.unregulated_inflow_name = "small"

plant1.average_unregulated_inflow = 0.0

session.model.add(plant1)

session.connect(upper1, plant1)

session.connect(plant1, lower1)

return upper1

[10]:

from pyltm import MarketStep

def add_market_step(session, name):

ms = MarketStep()

ms.name = name

ms.price = util.make_txy(

[

("2024-W01", [260]),

("2024-W20", [200]),

]

)

ms.capacity = util.make_txy(

[

("2023-W01", [150]),

]

)

return ms

[11]:

import pyltm

from pyltm import Wind

def add_wind(session, name, area):

wind = Wind()

wind.name = name

wind.capacity = pyltm.util.make_txy(

[

("2024-W01", [1, 2, 3, 4, 5, 6, 7, 8]),

("2024-W20", [3, 3, 3, 3, 3, 3, 3, 3]),

("2024-W40", [0, 0, 0, 0, 0, 0, 0, 0]),

("2024-W41", [30, 30, 30, 30, 30, 30, 30, 30]),

("2024-W43", [0, 0, 0, 0, 0, 0, 0, 0]),

]

)

session.model.add(wind)

session.connect(wind, area)

pass

[12]:

def create_basic_model(

name: str,

output_path: str,

sim_period: Txy,

hist_period: Txy,

):

session = LtmSession(name, ltm_core_path=ltm_core_path, overwrite_session=True)

sim = sim_period

hist = hist_period

# Explicitly set license file

gs = session.model.global_settings

gs.name = name

gs.output_path = output_path

gs.ltm_license_file_path = license_file

gs.delete_output_dir = False

gs.generate_output_dir = True

gs.simulation_period = sim

gs.historical_period = hist

gs.timesteps_per_week = 168

gs.default_spill_cost = 0.01

gs.default_load_penalty = 900.0

return session

def build_model():

session = create_basic_model(

"basic_model",

"testout_basic_model",

sim_period=util.make_txy_period("2024-W01", "2027-W01"),

hist_period=util.make_txy_period(

"2000-01-01T00:00:00Z", "2008-01-01T00:00:00Z"

),

)

add_default_inflow_series(session)

# areas

tev = add_area(session, "tev")

no2 = add_area(session, "NO2")

# DCLines

dc1 = add_dclines(session, "DC_TEV_NO2")

session.connect(tev, dc1)

session.connect(dc1, no2)

# Loads

load_tev = add_load(session, "load_tev")

load_no2 = add_load(session, "load_no2")

session.connect(load_tev, tev)

session.connect(load_no2, tev)

# Market step

ms1 = add_market_step(session, "market1")

session.connect(ms1, no2)

# Wind

add_wind(session, "windy", no2)

# NO2 Topology

upper1 = create_simple_topology(session)

session.connect(upper1, no2)

return session

def run_model(session: LtmSession):

# with build_model() as session:

with session:

try:

# Write model to disk, and automatically generate an output directory.

session._apimodule.dump_model("live_dump")

session.write_model()

# return

# Execute/run LTM/EMPS on the model

last_rc, results = session.execute_model()

# If last return code is not 0, then there was an error.

if last_rc != 0:

err = results[0]["log_file_contents"]

display_markdown(err)

else:

# Make plots from the results

generate_plots(session)

except Exception as e:

print(e)

raise (e)

[13]:

def go():

session = build_model()

run_model(session=session)

go()

INFO:LtmApiModel:(basic_model) Added object 'inflow/'

INFO:LtmApiModel:(basic_model) Added object 'inflow/'

INFO:LtmApiModel:(basic_model) Added object 'area/tev'

INFO:LtmApiModel:(basic_model) Added object 'area/NO2'

INFO:LtmApiModel:(basic_model) Added object 'dcline/'

INFO:LtmApiModel:(basic_model) Added object 'load/load_tev'

INFO:LtmApiModel:(basic_model) Added object 'load/load_no2'

INFO:LtmApiModel:(basic_model) Added object 'wind/windy'

INFO:LtmApiModel:(basic_model) Added object 'reservoir/upper1'

INFO:LtmApiModel:(basic_model) Added object 'reservoir/lower1'

INFO:LtmApiModel:(basic_model) Added object 'plant/plant1'

INFO:LtmApiModel:(basic_model) Not deleting output dir (testout_basic_model), as delete_output_dir: false, and has_generated_output_dir: false

INFO:LtmApiModel:(basic_model) LtmApiModel::maybe_generate_output_dir: output_path: /builds/energy/ltm/pyltmapi/docs/ltm-api/guides/live-ltm/testout_basic_model/2026-07-12-103744.405-EMPS-parallell

INFO:LtmApiModel:(basic_model) Using license file '/builds/energy/ltm/pyltmapi.tmp/CI_LTM_LICENSE_FILE'

INFO:Validator:(basic_model) Model validation succeeded

INFO:LtmApiModel:(basic_model) Writing model to path /builds/energy/ltm/pyltmapi/docs/ltm-api/guides/live-ltm/testout_basic_model/2026-07-12-103744.405-EMPS-parallell

INFO:InflowHandler:(basic_model) Writing inflow series

INFO:Validator:(basic_model) Model validation succeeded

INFO:LtmApiModel:(basic_model) Model executed successfully

area/tev

area/NO2

area/tev

area/NO2

INFO:LtmApiModel:(basic_model) Not deleting output dir (/builds/energy/ltm/pyltmapi/docs/ltm-api/guides/live-ltm/testout_basic_model/2026-07-12-103744.405-EMPS-parallell), as delete_output_dir: false, and has_generated_output_dir: true

INFO:LtmApiModel:(basic_model) Not deleting output dir (/builds/energy/ltm/pyltmapi/docs/ltm-api/guides/live-ltm/testout_basic_model/2026-07-12-103744.405-EMPS-parallell), as delete_output_dir: false, and has_generated_output_dir: true

[14]:

def open_and_modify_dump():

loaded_session = LtmSession(

"loaded_session", ltm_core_path=ltm_core_path, overwrite_session=True

)

with loaded_session:

loaded_session.load(filename="live_dump/model.json")

# Change unregulated inflow to 100 m3/sec

plant: Plant = loaded_session.model.get("plant", "plant1")

plant.average_unregulated_inflow = 100

# Remove wind

w: Wind = loaded_session.model.get("wind", "windy")

loaded_session.model.remove(w)

loaded_session.dump_model("live_dump_2")

pass

open_and_modify_dump()

INFO:LtmApiModel:(loaded_session) Loading model from file: live_dump/model.json

INFO:LtmApiModel:(loaded_session) LtmApiModel::maybe_generate_output_dir: output_path: /builds/energy/ltm/pyltmapi/docs/ltm-api/guides/live-ltm/testout_basic_model/2026-07-12-103800.568-EMPS-parallell

INFO:LtmApiModel:(loaded_session) Using license file '/builds/energy/ltm/pyltmapi.tmp/CI_LTM_LICENSE_FILE'

INFO:LtmApiModel:(loaded_session) Removing object 'wind/windy'

INFO:LtmApiModel:(loaded_session) Not deleting output dir (/builds/energy/ltm/pyltmapi/docs/ltm-api/guides/live-ltm/testout_basic_model/2026-07-12-103800.568-EMPS-parallell), as delete_output_dir: false, and has_generated_output_dir: true